In The Cattle Markets

Contributing Organizations

May 27, 2026

Bernt Nelson

Economist

American Farm Bureau Federation

Placements of Cattle on Feed up 6%

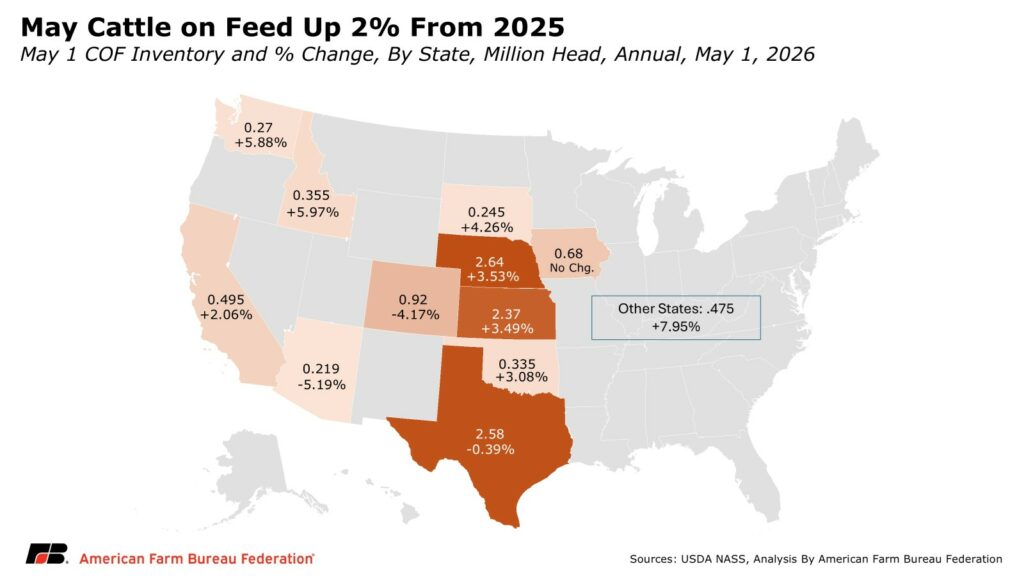

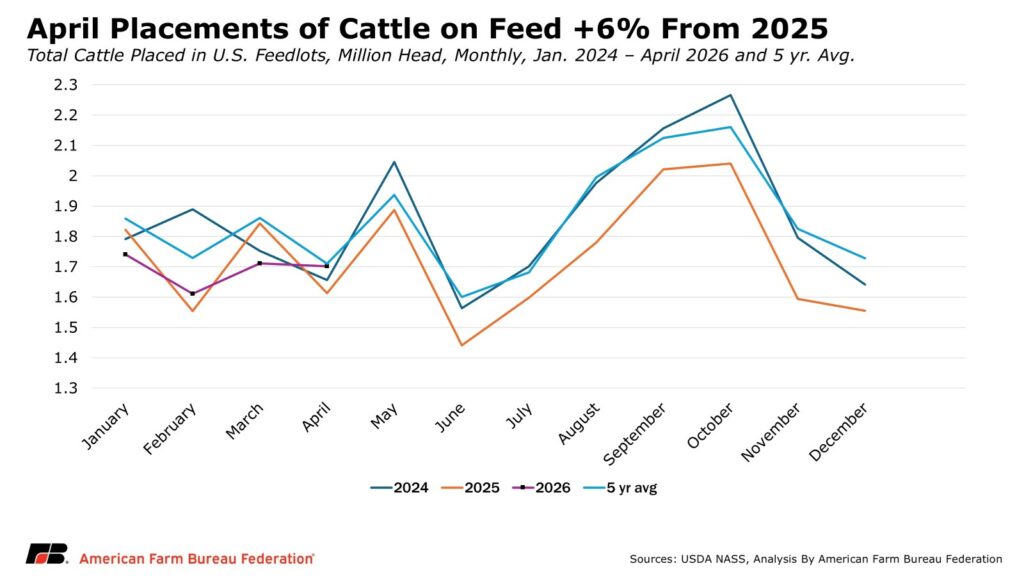

USDA’s latest Cattle on Feed report, released May 22, delivered slightly bearish news as higher-than-expected placements combined with lower marketings resulted in the first increase in the number of cattle on feed in 18 months. As of May 1, 2026, total cattle on feed in U.S. feedlots with a capacity of 1,000 head or more reached 11.6 million head, up about 2%, or 62,000 head, from May 2025. Placements totaled 1.7 million head, an increase of 89,000 head, or 6%, year over year, while marketings of fed cattle came in at 1.64 million head, roughly 10% lower than last year.

The report does not suggest herd expansion, but rather a modest uptick in the number of cattle being fed for beef production. Broader conditions in the cattle industry continue to limit expansion. According to Dr. Derrell Peel of Oklahoma State University Extension, more than 79% of the beef cow herd across the 26 largest cattle-producing states is currently affected by drought conditions, representing over 70% of the total U.S. herd. As drought persists, producers are dealing with elevated feed, hay, and water costs. These difficult conditions, along with continued record cash prices, may have encouraged farmers and ranchers to place heifers on feed that otherwise would have been retained as replacement females that could lead to long-term herd rebuilding.

At the same time, strong consumer demand continues to provide underlying support for cattle prices. Beef demand is expected to strengthen further during the summer grilling season, which could push prices for cattle and beef to new record highs. This sustained demand can be traced back to the COVID-19 pandemic, when beef became the preferred protein for many consumers cooking at home. USDA’s latest World Agricultural Supply and Demand Estimatesreport projects that total U.S. beef consumption in 2026 will reach 29.38 billion pounds. This represents an increase of 1.3%, or 390 million pounds, from 2025, and a 7.7% (approximately 1.8 billion pounds) increase compared to 2019 levels.

Looking ahead, significant uncertainty remains. Herd rebuilding decisions continue to be clouded by ongoing challenges, including persistent drought, elevated input costs and animal health risks such as New World screwworm. These factors are likely to keep production risks elevated even while beef demand remains strong, suggesting continued volatility in the cattle market in the months ahead.

The Markets

The bearish report generated a strong futures response on Friday, while cash markets remained more resilient. The 5-Area average weekly price for all grades of live, fed cattle was $260.49/cwt, down $2.36/cwt, or less than 1%, from last week but up $33.52/cwt, or almost 15%, from last year. This demonstrates that despite the bearish news, strong fundamentals continue to provide the framework for the cash cattle market:

- Cattle supplies are at a 75-year low

- Consumer demand is strong

- Herd rebuilding takes 2 years from the time a heifer calf is born, until it can have a calf of its own and create meaningful herd expansion.

- Approximately 70% of the total U.S. cattle inventory is under drought conditions

| Week of 5/22/26 | Week of 5/15/26 | Week of 5/23/25 | ||

| 5-Area Fed Steer | all grades, live weight, $/cwt | $260.49 | $262.85 | $226.97 |

| all grades, dressed weight, $/cwt | $410.24 | $411.07 | $361.74 | |

| Boxed Beef | Choice Value, 600-900 lb., $/cwt | $392.65 | $389.47 | $359.13 |

| Choice-Select Spread, $/cwt | $3.53 | ($0.45) | $11.61 | |

| 700-800 lb. Feeder Steer | Montana 3-market, $/cwt | — | $395.16 | — |

| Nebraska 7-market, $/cwt | — | $401.73 | $328.01 | |

| Oklahoma 8-market, $/cwt | $384.42 | $379.63 | $308.99 | |

| 500-600 lb. Feeder Steer | Montana 3-market, $/cwt | — | $487.56 | $408.89 |

| Nebraska 7-market, $/cwt | — | $499.95 | $392.18 | |

| Oklahoma 8-market, $/cwt | $476.99 | $474.87 | $383.21 | |

| Feed Grains | Corn, Omaha, NE, $/bu (Thursday) | $4.46 | $4.51 | $4.62 |

| DDGS, Nebraska, $/ton | $181.86 | $184.67 | $152.50 | |

Data Source: USDA-AMS Market News as compiled by LMIC